Over the past semester, I’ve been grateful for the opportunity to participate in BEMM129, an experimental course offered by the University of Exeter. The course was taught almost completely online; but what really made it different was the role of learners themselves in building the course. Prompts for learner comments were scattered throughout the course content, asking students to express their opinions on issues covered or provide examples. I was surprised by how much I enjoyed scrolling through these responses and learning about other people’s perspectives. I found these discussion spaces particularly useful at points in the course which discussed concepts like the circular economy. These ideas can sometimes feel a bit vague and difficult to grasp, and having a wide variety of examples discussed underneath really helped me to wrap my mind around the concepts.

Discussion prompts like this appeared throughout the course.

Another huge advantage of the learner contribution in this course was the variety of cultural perspectives that I was exposed to. The BEMM129 course alone had learners from dozens of countries on it – I won’t even mention the FutureLearn MOOC! Although I benefit from this diversity in regular university courses too, I found that, for whatever reason, people seemed to share more examples from their countries online. For example, I found Shiyan’s post about Vogue’s digital strategy in China incredibly interesting, and I doubt that I would have come across this information otherwise.

Just a few of the introductions from students.

One aspect of this course that I particularly enjoyed was having people comment on my blog posts. I found that some of the comments on my posts were really probing and asked great questions. Many people pointed out facts or examples that I hadn’t come across despite doing fairly extensive research for the posts. These interactions prompted me to dig deeper, even after the assignment was submitted. This is in stark contrast to my usual experience of submitting assignments, which is essentially just ‘finish it and forget about it’. I also really enjoyed being able to see what other people wrote in their responses to the same question. Reading other people’s work gave me ideas about how I could improve my own in the following blog post, especially with regard to using infographics, videos and more: I was amazed by the creativity of some people on the course!

In 2007, Mariam Naficy founded Minted. The idea was to sell stationery – greeting cards, wedding invitations, etc – online. Naficy had achieved e-commerce success during the Dot.com boom, founding Eve.com, an online cosmetics retailer that sold for $110 million (Shontell, 2011). However, it soon became clear that times had changed and simply bringing an offline product online was no longer enough. In response, Minted harnessed a new idea – crowdsourcing – to pivot to a different, more innovative business model.

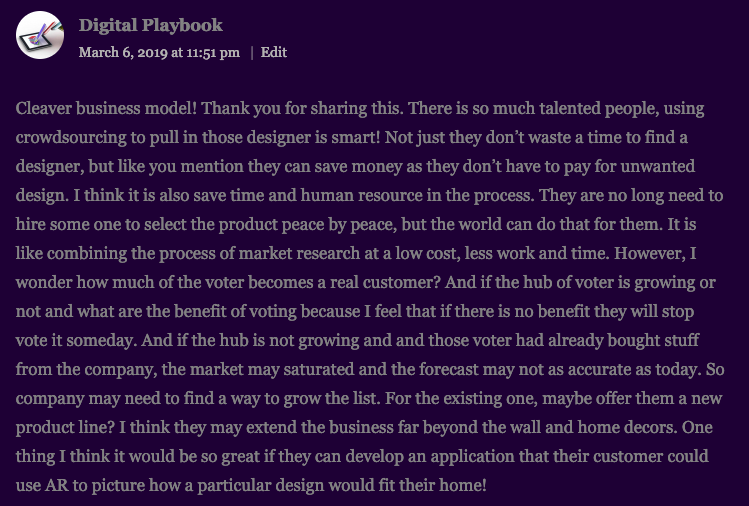

How Does It Work?

The Minted competition process (Infographic created on Canva.com)

Minted

announces an open competition calling for the public to submit designs for a

particular category of product – Save the Date cards, say. When the competition

closes, the submitted designs are posted online for people to vote for their

favourite. These votes are then fed into an algorithm which weights the votes

based on data about which demographics of voter are best able to predict sales

of that type of design (Carson, 2019). Based on this weighting, the algorithm

selects winners, whose designs are then sold on Minted.com.

Minted

is valued at over $700 million, with annual revenues increasing at 39%

year-on-year (Carson, 2019). The secret behind the startup’s success lies in

its innovative business model that gives Minted several advantages over its

competitors.

1. Costs are Low

Because Minted crowdsources designs, the company’s costs are incredibly low. They don’t have to hire in-house designers and no longer expend money and energy on signing existing brands to sell on their platform. They also don’t have to pay designers unless their designs are selected – this is different from working with freelancers, who would charge for a project regardless of whether their work is used. On Minted, winning designers get paid a prize fee of between $100-$3000 and earn a 6% commission on net sales of their product (“About us | Minted”, 2019). This ends up far cheaper for Minted than hiring in-house designers, working with freelancers, or signing brands. Mariam Naficy further explains how crowdsourcing fuels Minted’s business in the video below.

Source: Fox Business (2015)

2. Products are Validated by Design

The Minted business model (“About us | Minted”, 2019).

Thanks to the clever pairing of crowdsourced voting and data-powered algorithm, Minted’s products are validated before a penny is spent on development. Minted has a near-guarantee that every new product they release is going to sell well. With estimates of new product failures at over 80% (Kocina, 2017), this is a huge advantage. Whereas traditional greeting card companies may have to go with their gut on new product launches or invest thousands of dollars into market research, Minted has the eyes and ears of thousands of consumers at their disposal, every day, completely free.

3. No Inventory is Wasted

Source: Morgans (2013)

Finally, the third distinguishing feature of Minted’s business model is the fact that products are produced only when they are ordered. Because the majority of products on the site are personalisable, they are printed only when somebody pays for them. Although this presents logistical challenges in delivering quick turnarounds, this model ensures that nearly no inventory is wasted. This means that even if a product makes it into production but doesn’t sell well, Minted loses nothing but the designer’s prize fee, because no stock will have been produced.

Is Minted’s Business Model Sustainable?

The empire may or may not eventually fall, but for now, Minted has built a highly profitable enterprise based on a clever digital business model. It has, in fact, proved so successful that Minted is no longer just a stationery company: it now applies the same model to wall art and home decor, and recently raised $208 million in Series E funding for expansion into other markets (Clark, 2018).

Of course, a potential problem with running a business based on crowdsourcing is the risk of losing the crowd. Minted is dependent on its online community in every stage of its business model. If Minted’s users were to stop entering their competitions and voting for their favourite designs, the company would be in trouble. How likely is that to happen? Well, Minted has thousands of engaged members who love the service and feel it enables them to pursue their creative hobbies more seriously than would otherwise be possible (Birstengel, 2018). However, some designers are not huge fans.

In an article on her blog, designer Kiffanie Stahle discouraged artists from entering Minted competitions, claiming that Minted’s terms and conditions are unfair in taking away artists’ copyright of their own designs (Stahle, 2018). Many believe that the entire concept of crowdsourcing is unethical because it involves people doing work for for-profit organisations for free or at a fraction of the price the company would otherwise have to pay (Schmidt, 2013). If this way of looking at crowdsourced design catches on with its community, Minted’s business will be in danger of collapse. The video below further discusses some of the ethical concerns associated with crowdsourcing.

Source: Dawson (2012)

The

empire may or may not eventually fall, but for now, Minted has built a highly

profitable enterprise based on a clever digital business model. It has, in

fact, proved so successful that Minted is no longer just a stationery company:

it now applies the same model to wall art and home decor, and recently raised

$208 million in Series E funding for expansion into other markets (Clark,

2018).

Naficy, M. (2015, November 25). How Minted’s CEO Kept Her Paper Design Company From Folding (L. Schiller, Interviewer) Fortune. Retrieved from http://www.fortune.com

Of all the industries affected by the last decade’s shift to digitisation, perhaps none have been so completely turned upside-down as banking. Thanks to changing consumer preferences, the rise of challenger banks and FinTech initiatives, brick-and-mortar banks must race to keep pace with new developments. Some have managed these changes more effectively than others.

Business Insider Intelligence (2018)

One organisation that has done an exemplary job of managing the migration to digital is the Royal Bank of Scotland Group, encompassing RBS, Natwest and Coutts banks, among others (“Our brands”, 2019). Just a decade ago, the banking group was at the centre of the 2008 recession in the UK, being bailed out by the government for a cool £45 billion (Davies, 2018). In 2018, RBS’ CEO Ross McEwan described the group’s progress since then as ‘the biggest turnaround in corporate history’ (Arnold, 2018). So what’s changed?

RBS Group has taken the digitisation of banking seriously, staying ahead of the curb with digital initiatives designed to keep it relevant in the face of digital challenger banks like Monzo and Revolut. RBS has responded by investing heavily in its own digital banks. Currently under development are at least 6 stand-alone digital banks with varying focuses (Arnold, 2018). Already in beta is Mettle, a digital-only bank account for SMEs. Among the other projects in the works is Bó, a customer-facing Monzo competitor which is set to take on 1 million current Natwest customers upon its launch (Smith, 2018).

Mettle, RBS’ digital-only bank account for business (Mettle, 2018).

In addition, RBS Group has launched a number of innovative digital services for its current clients. Natwest recently introduced Esme Loans, a digital lending platform for small businesses. Even private bank Coutts, the seventh oldest bank in the world, is taking a leap of faith into the digital world with Coutts Connect, a social network for its’ high-end clients (Rach, 2018). The network facilitates online networking between clients who share business interests. If proven successful, this could mark a significant shift in banking, traditionally a very private industry.

As well as developing new technologies in-house, RBS Group places itself in an ideal position for acquisition of promising FinTech projects. The group does a lot to support entrepreneurship, from its Entrepreneur Accelerator offering mentorship and funding to early-stage startups, to its conversion of a cash delivery centre in London into a tech start-up campus, complete with a networking space inside the old vault (“RocketSpace to open London campus for tech startups thanks to RBS”, 2016). These initiatives keep RBS Group current and up to date on trends in FinTech, allowing them to stay ahead of the curb.

RocketSpace, the start-up campus, based inside a former RBS cash delivery centre (LOM, 2017)

Of course, digitisation does present challenges. In 2012, a major computer failure descended Natwest into chaos, causing weeks of disruption to services including viewing account balance, foreign cash withdrawals and making mortgage payments (“RBS fined £56m over computer failure”, 2014). In response to the digital crisis, Natwest deployed human power: 1,200 branches extended their opening hours and phone staff was doubled in an attempt to manage customers’ access to their cash (Adetunji, 2012). Some failures are inevitable in the introduction of new technologies. Although costly, incidents like this are likely to continue to become less common as banking continues to shift its core focus to digital. However, they do also call into question the reliability of mobile-only banks, who do not have physical branches to fall back on in the event of a disruption to online services.

Another challenge that brick-and-mortar banks are facing is the impact of digitisation on the physical side of the business. In 2014, RBS announced that its branch transactions had fallen by 30% in the previous 4 years (“RBS to close 44 branches across UK”, 2014). Like most other high street banks, RBS is in the process of dramatically cutting its physical locations in the coming years. However, the approach they are taking is different from most.

Moneybright on Flickr (2014)

Lloyds Bank recently announced that it is axing over 6000 jobs in its shift to digitisation (Hawker, 2018). It defended its decision with promises of over 8000 new digital roles; however, this will inevitably leave its current employees, who lack digital training, in the cold. In stark contrast, RBS Group plans to cut fewer than 800 jobs, despite 162 branch closures planned for the coming years (“RBS to cut 162 branches and 792 jobs”, 2018). How is that possible? RBS plans to retain the vast majority of its current employees, re-training them for digital roles. Natwest has already launched its Data Academy, a programme open to all of RBS Group’s 70,000 staff, designed to train them to understand and harness the power of data (“NatWest becomes first UK bank to launch Data Academy”, 2019).

Time will tell whether RBS Group’s ventures into digitisation will pay off, or if the 50-year-old banking group is doomed to lose out to the industry’s new entrants. However, it’s safe to say that RBS has made a calculated move to embrace digitisation in a bid to not get left behind.

Last year, I worked at a London technology start-up as a Growth Marketer. To make a long story short, growth is a data-driven approach to marketing that uses trial and error to find the best way to get new users and keep them onboard (Nelson, 2017). Growth (versus marketing) is a pretty new idea because, without the data collection and analysis software available today, it just wouldn’t be possible.

In my job, I relied heavily on some amazing technologies. For example, to manage Pay Per Click ads, I used a tool called AdEspresso. I could upload a few pieces of copy and images, select my targeting, and the programme would create hundreds of variations of PPC ads. It would then analyse how well each converts over time and automatically allocate budget according to which ads performed best.

Artificial intelligence and machine learning are really good at spotting patterns in data and responding to them. However, they’re not so good at the creative side of things. In the future, AI-based programmes may be able to write optimised copy and create images themselves, without the marketer having to do anything but approve the ad. Currently, though, this just isn’t something technology can do anywhere close to the level of humans (Ford, 2018). Many experts believe that some creative input will always be necessary, seeing automation software as more of an assistant than a replacement for humans (Kreimer, 2017).

As an assistant, however, the technology can help us optimise our creativity. MarketMuse is a start-up that helps marketers optimise their content marketing with AI. The software scours the internet for topics relevant to a business, identifies gaps they can fill with effective content marketing. It can also analyse your existing articles to see how they compare to similar ones in terms of SEO and content (“AI Marketing Tool Suite”, 2019). With the incredible volume of information on the internet, a tool like this can really put a company’s content marketing on the map. This is an incredible example of how technology can be harnessed to help us direct and optimise our very human skill of creativity.

Tools for automation of processes like bidding for PPC ad space, search engine optimisation and even optimising content are continually making marketers’ jobs more streamlined and efficient. These tools allow marketers to focus on the things that aren’t as easily automated: strategy and creativity. All competing companies will have access to more or less the same technologies, but the elements that distinguish those who get ahead are and will be human.

{kind=link}